CHAPTER 13 BANKRUPTCY ATTORNEY

What is Chapter 13 Bankruptcy?

A Chapter 13 Bankruptcy is a reorganization of your debts into a 3-5 year payment plan. This is also referred to as a wage earner’s plan. Depending on the circumstances, the debtor will repay all or a portion of their debt through this plan.

How does Chapter 13 Bankruptcy work?

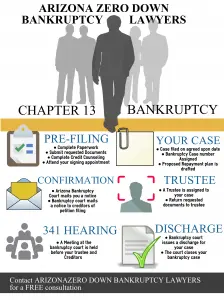

You will first need to gather all documents related to your finances. The timespan you will have to provide will vary by the type of document. You will either submit these documents to your attorney who will prepare your petition, or if you are filing pro se, you must prepare the petition yourself. You or your attorney will then file the petition.

Along with the petition, you must also file schedules of assets and liabilities, a schedule of current income and expenditures, a schedule of executory contracts and unexpired leases, and a statement of financial affairs. Once all this is filed, you will be assigned a bankruptcy trustee. The trustee will examine your documents to make sure you didn’t fail to disclose any assets and that your plan is feasible.

Within 14 days of filing the bankruptcy petition, you must also submit a proposed repayment plan. Whether or not your plan has been approved yet, you must begin payment within 30 days of filing your case. You will then have to attend a 341 Meeting of Creditors and a confirmation hearing for your plan. Once all these steps, and the online credit counseling courses are completed, the creditor simply must continue making their payments until the plan is completed.

Is Chapter 13 better than Chapter 7?

This depends on your situation. If you have stable income and want to keep your assets, Chapter 13 is your best bet. If you have low or sporadic income and are looking to surrender assets that you can no longer afford the payments on instead of retain them, a Chapter 7 may be better for you.

Which Chapter is the best to keep my home? Why?

If you are behind on your mortgage payments and facing foreclosure, a Chapter 13 allows you to spread out the arrearages over the life of your payment plan. Once you file your bankruptcy petition, an automatic stay of protection goes into effect. The stay prevents your mortgage provider from foreclosing on your home. The stay remains in effect until you complete your payment plan or your case is dismissed.

Will I lose any of my property in a Chapter 13?

Generally, you can keep all of your property in a Chapter 13. This includes properties that are above the exemption amounts in a Chapter 7. Examples include $6,000 equity in one vehicle, $150,000 in your home, and $6,000 in furniture and home goods. Exemptions will vary by state and you should check with an attorney to see which state’s exemptions you will use.

Do I need an attorney to file Ch 13?

There is nothing legally preventing you from filing a Chapter 13 bankruptcy on your own. However, less than 1% of pro se (self) Chapter 13 filers gets their plan approved. The success rate for getting plans approved by filers represented by attorneys is 55%.

Will people know if I file Chapter 13?

While bankruptcies are a matter of public record, for the most part, only your creditors will be notified of your bankruptcy. Your employer or landlord may also be notified in certain situations. Family and friends will likely only learn of your bankruptcy if you inform them of it.

What debts are dischargeable in a Ch 13 bankruptcy?

Unsecured debts such as credit cards and medical bills are dischargeable in both a Chapter 7 and a Chapter 13. Some debts can be included in only a Chapter 13, and not a Chapter 7. These include debts incurred to pay non-dischargeable taxes, debts from property settlements in family law proceedings, and debts from willful and malicious damages to property. You can also discharge junior mortgages on your home if you owe more on your home than it is worth.

How much does it cost to file a Ch 13 bankruptcy?

The court filing fee for a Chapter 13 bankruptcy is $310, and the fees for credit counseling courses vary. While attorney’s fees for a Chapter 13 are typically more expensive than for a Chapter 7, they can be worked into your plan. Your attorney will likely require some payment up front, which will vary by region and office.

How long does a Chapter 13 bk last?

A Chapter 13 bankruptcy lasts 3-5 years. If you are below the median income level for your state based on your family size, your plan will be 3 years. If you are above the median income level, your plan will be 5 years.

What are the advantages of a Chapter 13 bankruptcy?

A Chapter 13 gives you the opportunity to catch up on payments on your house or vehicle. In a Chapter 13, you can pay off any arrearages over 3-5 years, while a Chapter 7 bankruptcy will only provide you with about 3-5 months to pay off these debts. Chapter 13 also has a provision for consumer debts that will protect any cosigners. Depending on your income and the amount of unsecured debt you have, you may not be required to pay off the entirety of your debt.

What are the disadvantages of a Chapter 13 bankruptcy?

One of the obvious advantages of a Chapter 13 is that you actually have to pay some or all of your debts, while they are merely discharged in a Chapter 7. There is also the riskiness of drafting your plan and experiencing a change in income and not being able to make your payments anymore. You can risk your case being dismissed if this happens.

What is a Chapter 13 discharge?

A chapter 13 discharge is the completion of you Chapter 13 Bankruptcy. This can only occur when you have completed all the steps of the bankruptcy and completed your payment plan. A Chapter 13 bankruptcy can’t continue past 5 years- so if there are any unsecured debts remaining at the end of your 5 year plan, they will be wiped out.

When will my debt be discharged in a Ch 13 bk?

Your case can only be discharged once you have completed your credit counseling courses, attended your 341 Meeting of Creditors, and made the final payment in your Chapter 13 plan.

PHONE

602-609-7000

HOURS:

Monday-Thursday 8:00 AM – 7:00 PM

Friday: 8:00 AM – 6:00 PM

Evening and Weekend hours available by appointment

EMAIL

[email protected]